Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

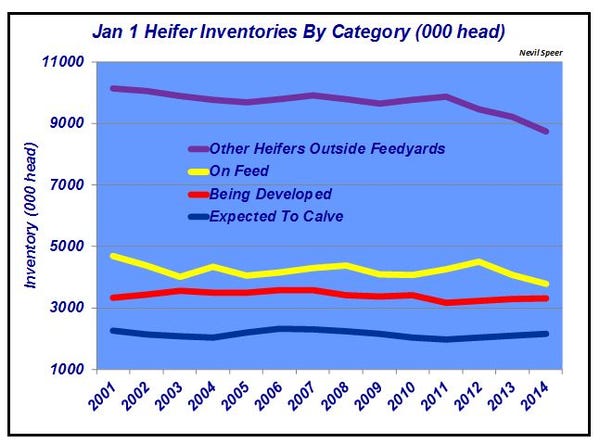

Replacement heifer figures have remained relatively steady over time, despite declining cow numbers. With herd rebuilding beginning in earnest in the U.S., it signals a market tussle between cow-calf producers wanting to retain heifers and margin operators who need cattle.

March 19, 2014

This week’s Industry-At-A-Glance reflects Jan. 1 heifer inventory by respective category. Consideration of some of the specific inventory trends possesses some important implications.

• The annual inventory of beef replacement heifers has stayed relatively constant over time. That reality underscores the overwhelming contribution of beef cow slaughter (vs. a slowdown in heifer retention) when explaining the declining cow inventory.

• Declining cow inventory means smaller calf crops, which cuts into the available supply of feeder heifers for both stocker operators and feedyards. So, while replacement heifers have remained relatively steady, these remaining categories (other heifers and those on feed) have notably declined.

Therein enters the challenges for the industry. There’s seemingly an increasing appetite for cowherd rebuilding, which will occur from both a slowdown in cow liquidation and greater retention of heifers for the purpose of being put back into the cowherd. However, increased retention further confounds an already tight feeder cattle supply. That inherently creates a market tussle between cow-calf producers wanting to retain heifers and margin operators who need cattle.

How do you see this shaping up in the next several years? What types of prices will we begin to see for heifers across the categories? Which sector will ultimately win out? Leave your thoughts below.

How do you see this shaping up in the next several years? What types of prices will we begin to see for heifers across the categories? Which sector will ultimately win out? Leave your thoughts below.

More articles to enjoy:

Ag Lender Advises Cattlemen To Lock In Interest Rates Now

The Beef Industry's Ultimate Goal Should Be A Satisfied Consumer

Enter The Greeley Hat Works Why I Ranch Essay Contest

120+ Romantic Ranch Photos Submitted By Readers

More Herd Expansion Perspective

You May Also Like

Enter a zip code to see the weather conditions for a different location.

.png?width=300&auto=webp&quality=80&disable=upscale)