Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

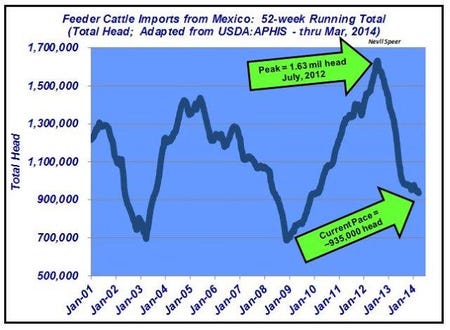

The combination of fewer available heifers to graze and feed in the U.S., and fewer cattle being sourced from Mexico, makes for an especially tight supply outlook in the coming months.

April 1, 2014

A tight supply of cattle is a perpetual story. And as noted several weeks ago, tight supply is exacerbated in 2014 because of an especially tight supply of cattle in the “other heifers” category. Meanwhile, some of the shortfall in domestic supply has been buffered by increased flow of feeders from Mexico.

The need to maintain occupancy at the feedyard level was favorably matched by willing sellers because of drought in Mexico. The trade peaked in July 2012 with an annual import rate of 1.63 million head. However, since that time, there’s been a sharp decline – the current rate is off by more than 40% and has slowed to 935,000 head/year.

When one considers both the fewer number of available heifers to graze and feed, and the fewer number of cattle being sourced from Mexico, it makes for an especially tight supply outlook in the coming months. That squeeze could be significant as the U.S. beef industry markets through the current wave of placements and the hunt for replacements begins in earnest.

How do you see these factors shaping the feeder market in the second half of the year? Will tight supply make the market run even higher? What impact might that have on long-term strategies among feedyards to source cattle? Leave your thoughts below.

How do you see these factors shaping the feeder market in the second half of the year? Will tight supply make the market run even higher? What impact might that have on long-term strategies among feedyards to source cattle? Leave your thoughts below.

More articles to enjoy:

Despite Record Prices, Push The Pencil For The Best Selling Option

9 Nifty New Products For Cattle Producers

Leachman’s Industry Game Plan: Work Together To Move Forward

Grass-Fed Vs. Grain-Fed Ground Beef -- No Difference In Healthfulness

You May Also Like

Enter a zip code to see the weather conditions for a different location.